Welcome to the Hardcore Husky Forums. Folks who are well-known in Cyberland and not that dumb.

Greenspan says dump Dodd-Frank

HFNY

Member Posts: 5,599

in Tug Tavern

And increase capital requirements. I agree:

ft.com/cms/s/0/4d55622a-44c8-11e5-af2f-4d6e0e5eda22.html#axzz3jCqRUKBI

ft.com/cms/s/0/4d55622a-44c8-11e5-af2f-4d6e0e5eda22.html#axzz3jCqRUKBI

Comments

-

Note it may require answering two survey questions to read the full article but giving you basement dwellers full disclosure so you don't complain (or can't complain much since I know you will anway....water is wet).

-

Lots of good nuggets at the end of his opinion piece:

"An important collateral pay-off for higher equity in the years ahead could be a significant reduction in bank supervision and regulation.

Lawmakers and regulators, given elevated capital buffers, need to be far less concerned about the quality of the banks’ loan and securities portfolios since any losses would be absorbed by shareholders, not taxpayers. This would enable the Dodd-Frank Act on financial regulation of 2010 to be shelved, ending its potential to distort the markets — a potential seen in the recent decline in market liquidity and flexibility.

Well-capitalised banks need to be less fettered in their primary economic function: to assist in the directing of the nation’s scarce savings to fund our most potentially productive investments. Funding cutting-edge capital investments will engender growth in national productivity and standards of living."

-

A banking guy that oversaw a period of deregulation that preceded a financial collapse wants less regulation. Shocking.

-

A fag who pimped out of his house is who I want writing laws2001400ex said:A banking guy that oversaw a period of deregulation that preceded a financial collapse wants less regulation. Shocking.

-

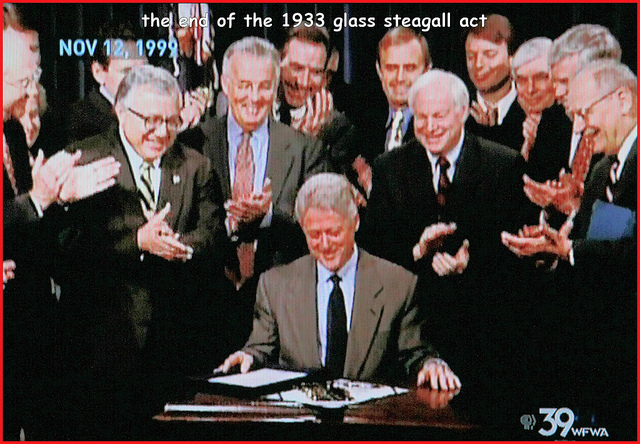

How about start by re-instating Glass-Stiegel. Shit never would have happened in the first place.

-

You may not remember but Clinton was the President when Glass Stegall was repealed:

2001400ex said:

2001400ex said:A banking guy that oversaw a period of deregulation that preceded a financial collapse wants less regulation. Shocking.

-

People also forget that the Clinton administration oversaw the destruction of home lending standards that planted the seed for the subprime crisis.

-

who knew that forcing banks to issue mortgages to people who didn't qualify would be a problem? the relaxed standards were also used by investors to over extendPurpleJ said:People also forget that the Clinton administration oversaw the destruction of home lending standards that planted the seed for the subprime crisis.

-

It made for great campaign rhetoric. Kind of like the idea of "free" healthcare. Now all the fucktards in my generation are jumping on the Bernie train for "free" college education. Never mind the fact that they already went deep into debt for their degrees in Barista Studies. They should really start teaching basic econ in high schools again.RaceBannon said:

who knew that forcing banks to issue mortgages to people who didn't qualify would be a problem? the relaxed standards were also used by investors to over extendPurpleJ said:People also forget that the Clinton administration oversaw the destruction of home lending standards that planted the seed for the subprime crisis.

-

Greenspan is a dumbass and should not be listened to on any topic of importance. That's how wrong and dumb he was about the 2008 financial crash.

Alan Greenspan, once viewed as the infallible architect of U.S. prosperity, was called on the carpet yesterday, pilloried by a congressional committee for decisions that contributed to the financial crisis devastating world markets.

http://www.washingtonpost.com/wp-dyn/content/article/2008/10/23/AR2008102300193.html

The former chairman of the Federal Reserve said the crisis had shaken his very understanding of how markets work, and agreed that certain financial derivatives should be regulated -- an idea he had long resisted.

OP is akin to listening to Dick Cheney and Paul Wolfowitz on Middle East policy. Their failures should discredit them.